An in-depth economic analysis of multinational contract manufacturing in Ireland.

Ireland's macroeconomic data has long been notorious for its volatility, but recent figures from the Central Statistics Office (CSO) have once again thrust the phenomenon of "phantom exports" back into the spotlight. Driven by the accounting structures of global pharmaceutical and technology giants, these exports are growing rapidly, distorting Gross Domestic Product (GDP) and creating a widening disconnect with the real domestic economy.

Officially classified as contract manufacturing (or "goods for processing"), these transactions occur when a multinational company headquartered in Ireland contracts a third-party factory abroad to manufacture products. While the raw materials and finished goods never physically enter or leave Ireland, they are recorded as Irish exports because the economic ownership of the intellectual property (IP) and inventory remains with the Irish-registered entity.

The 2025-2026 Export Divergence

The scale of these offshore transactions has reached historic proportions. In late 2025, multinational corporations aggressively "front-loaded" global contract manufacturing exports—shipping stockpiles of pharmaceuticals and high-tech components from production hubs in Asia and Europe directly to the United States. This preemptive surge was designed to hedge against potential US tariff policies, resulting in a dramatic spike in Ireland's reported export figures.

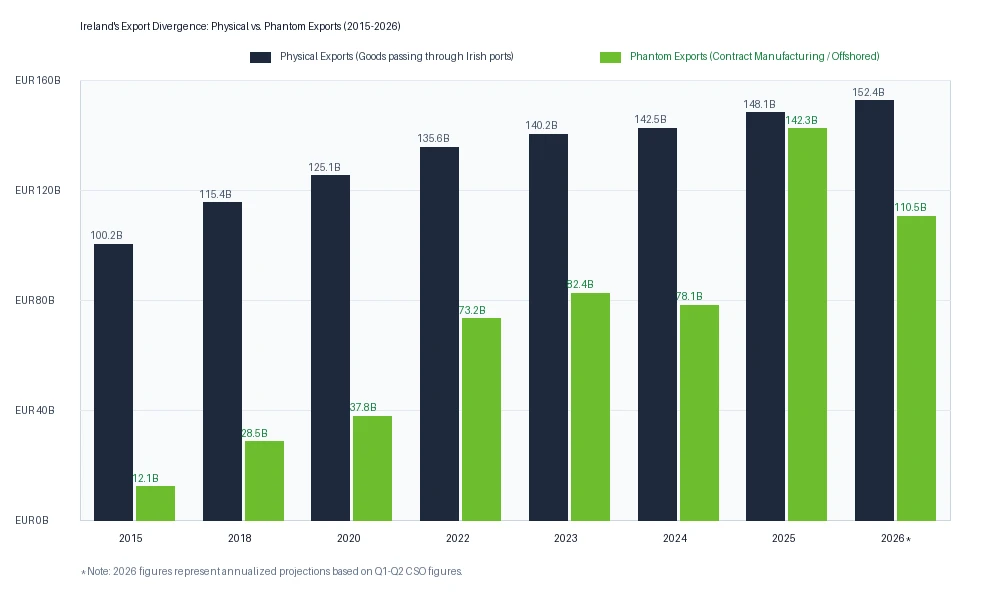

While this front-loading trend has started to wind down in mid-2026, the volume of contract manufacturing remains a massive component of the nation's ledger. To illustrate this divergence, Priya Life Science has compiled the historical export data, mapping the growth of physical goods departing Irish ports against offshore contract manufacturing:

Figure 1: Grouped bar chart comparing physical goods departing Irish ports vs. offshore contract manufacturing (Billion EUR) from 2015 to 2026.

As shown in the data, while physical exports have grown at a steady, predictable rate, contract manufacturing has experienced explosive volatility. In 2025, contract manufacturing spiked to an unprecedented €142.3 billion, briefly rivaling the value of all physical goods physically shipped from the island. Annualized data for 2026 shows a stabilization at approximately €110.5 billion, indicating that while the panic-buying has eased, the offshore bookkeeping model remains deeply embedded.

Why the Biopharma Sector Drives this Model

Ireland is the European headquarters for 19 of the top 20 global pharmaceutical companies. Giants such as Pfizer, AbbVie, Johnson & Johnson, and Sanofi maintain extensive physical manufacturing footprints in Dublin, Cork, Waterford, and Limerick. However, the commercial structure of these companies means that Ireland also acts as the global hub for their intellectual property.

When an Irish subsidiary of a pharmaceutical multinational contracts a manufacturing facility in Germany, Puerto Rico, or Singapore to produce a biologic drug, the transaction is routed through Ireland. The Irish entity purchases the raw materials, retains ownership of the active pharmaceutical ingredient (API) throughout the process, and records the final sale as an Irish export. Consequently, a drug manufactured in Germany and sold in France is officially registered as an Irish biopharma export, adding to the "phantom" column of Ireland's trade balance.

The GDP Illusion and GNI*

The core problem with this arrangement is that it creates a false impression of Irish economic health. When phantom exports surge, headline GDP rises. Yet, because the physical manufacturing occurs elsewhere, this growth does not translate into new manufacturing jobs, factory expansions, or local wage growth in Ireland. The profits simply accumulate in the Irish corporate registry before being repatriated or reinvested globally.

To cut through this statistical noise, economists and the Irish Government rely on alternative metrics:

- Modified Gross National Income (GNI*): This measure strips out the depreciation of intellectual property, R&D activities, and the aircraft leasing sectors to show the actual size of the Irish economy.

- Modified Domestic Demand (MDD): This index measures personal spending, government consumption, and domestic investment, providing a clearer view of real-world economic activity.

While reported GDP spiked in late 2025 due to contract manufacturing, Modified Domestic Demand grew by a modest 2.4%, highlighting that the domestic economy is growing steadily, completely insulated from the wild swings of multinational bookkeeping.

Strategic Vulnerabilities and the Tariff Threat

The reliance on phantom exports exposes Ireland to major external vulnerabilities. The implementation of the OECD Pillar Two agreement, which establishes a 15% global minimum corporate tax rate, has reduced some of the incentives for routing offshore manufacturing profits through Irish entities. Furthermore, changes in US trade policies could penalize goods based on their physical country of origin, regardless of their economic registration in Ireland, complicating corporate structures.

For Irish policymakers, the message is clear. While these multinational accounting flows provide substantial corporate tax revenues, they should not be confused with organic domestic growth. Building long-term economic resilience requires continued investment in local infrastructure, skills, and native startups, ensuring that Ireland's economic foundation remains secure—even if the phantom exports disappear.